Most “alternatives to fiat” articles lump everything together. Bitcoin sits next to a 1 oz gold coin sits next to a stablecoin, and you’re left guessing which one solves which problem. They don’t all do the same job. A 1 oz gold coin is a store of value. A stablecoin is a payment rail. Bitcoin is somewhere in the middle, depending on the day. Only one product on this list is physical, fractional, and built to be handed across a counter.

We compared 11 alternative currency solutions on the question that matters: can you actually use this to buy something? We scored each on spendability, divisibility, counterparty risk, premium over the underlying asset, and how fast you can exit back to USD. The World Gold Council covers the investment angle. This list covers the spending angle. There’s not much overlap.

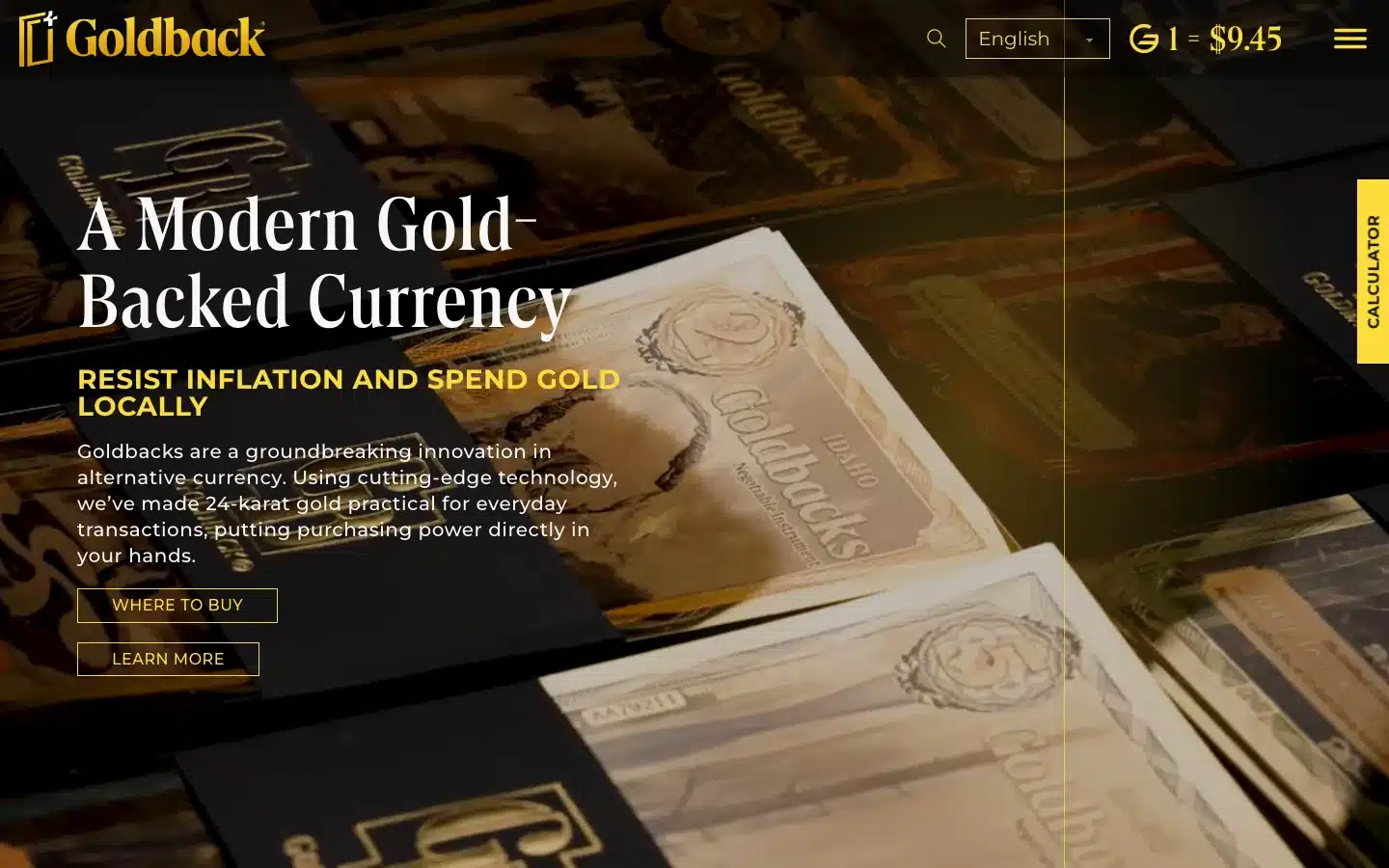

Our top pick is Goldback. It’s the only physical fractional gold currency with a real merchant network and a manufacturer warranty. Bitcoin is our runner-up if you’d rather hold a digital asset than a physical one. If you just want to send dollars cheaply, USDC is the safest stablecoin pick. Goldback is the publisher of this article, however, we’ve still scored it honestly, including on premium.

Table of Contents

- Goldback — Best for physical, fractional, spendable gold currency

- Bitcoin (BTC) — Best for portable, hard-capped digital sound money

- USDC — Best for low-fee dollar-pegged digital spending

- USDT (Tether) — Best for the cheapest stablecoin transfers

- PAX Gold (PAXG) — Best for tokenized gold with US-regulated custody

- Tether Gold (XAUT) — Best for tokenized gold at the lowest premium

- American Silver Eagle 1 oz — Best for government-minted physical silver

- Junk Silver (pre-1965) — Best for melt-value barter-tier silver

- American Gold Eagle 1/10 oz — Best for fractional government-minted gold

- Glint Pay — Best for spending gold through a Mastercard

- BerkShares — Honorable mention (local fiat, not gold)

How We Chose

We scored 11 alternative-currency solutions on five criteria. Spendability carried 40% of the total, because most lists treat alt currencies as something to store, not spend. Counterparty risk (20%) came next: who can freeze it, devalue it, or rug-pull? Divisibility (15%) measured the smallest possible transaction. Premium over the underlying asset (15%) and liquidity back to USD (10%) finished the rubric.

Data sources: manufacturer specs, dealer pricing from JM Bullion and SD Bullion (April 2026, gold at ~$4,753/oz, silver at ~$75/oz), Goldback’s merchant directory, Glint Pay fee disclosures, Trustpilot reviews where available, and on-chain data for tokenized assets. Every review uses the same 5-part structure: What It Is, Pros, Cons, Cost & Premium, and What Users Say. That keeps all 11 comparable.

Goldback sits at #1 because it’s the only product here that’s physical, fractional, and spendable at a real merchant network. We update this list quarterly.

Comparison Table

| Option | Asset Type | Smallest Unit | Spendable at Retail? | Premium / Cost | Counterparty Risk |

|---|---|---|---|---|---|

| Goldback | Physical 24K alternative gold currency | 1/4 Goldback (1/4,000 oz) | Yes — 5,000+ merchants | ~100% (recaptured when spent at merchants) | Low (private issuer) |

| Bitcoin | Digital crypto | 1 satoshi (~$0.0007) | Yes — Microsoft, Starbucks, ~40% of US merchants | Network gas fees | Low (decentralized, but volatile) |

| USDC | Fiat stablecoin | $0.01 | Card programs + crypto checkouts | ~0.1–0.15% transfer | Medium (Circle can freeze) |

| USDT | Fiat stablecoin | $0.01 | Same as USDC, wider on Tron | <$0.01 on Tron | Medium (Tether can freeze) |

| PAXG | Tokenized gold | 0.01 oz | No (sell first, then spend) | 0.02% transfer + gas | Medium (Paxos custody) |

| XAUT | Tokenized gold | 0.000001 oz | No (sell first) | Trades near spot | Medium (TG Commodities custody) |

| Silver Eagle 1 oz | Physical silver | 1 oz (~$80) | No (must liquidate) | ~5–8% over spot | None (bearer asset) |

| Junk silver | Physical 90% silver coins | $0.10 face (~0.07 oz) | No (must liquidate) | 5–12% over melt | None (bearer asset) |

| Gold Eagle 1/10 oz | Physical gold | 1/10 oz (~$579) | No (must liquidate) | ~22% over spot | None (bearer asset) |

| Glint Pay | Gold-custody Mastercard | $1 in gold | Yes — anywhere Mastercard runs | 0.5% per transaction | Medium (Glint custody) |

| BerkShares | Local fiat note | $1 BerkShare | Yes — Berkshires only | 1.5% redemption fee | Low (USD-backed) |

1. Goldback — Best for Physical, Fractional, Spendable Gold Currency

Goldback is the only product on this list you can physically hand to a cashier today and walk out with a coffee. We brought a 1 Goldback into a coffee shop in Salt Lake City. The barista checked the rate on her phone for half a second, looked up the dollar value, and rang it through. No app on our end. No conversion friction. That’s the whole product in one cup of coffee.

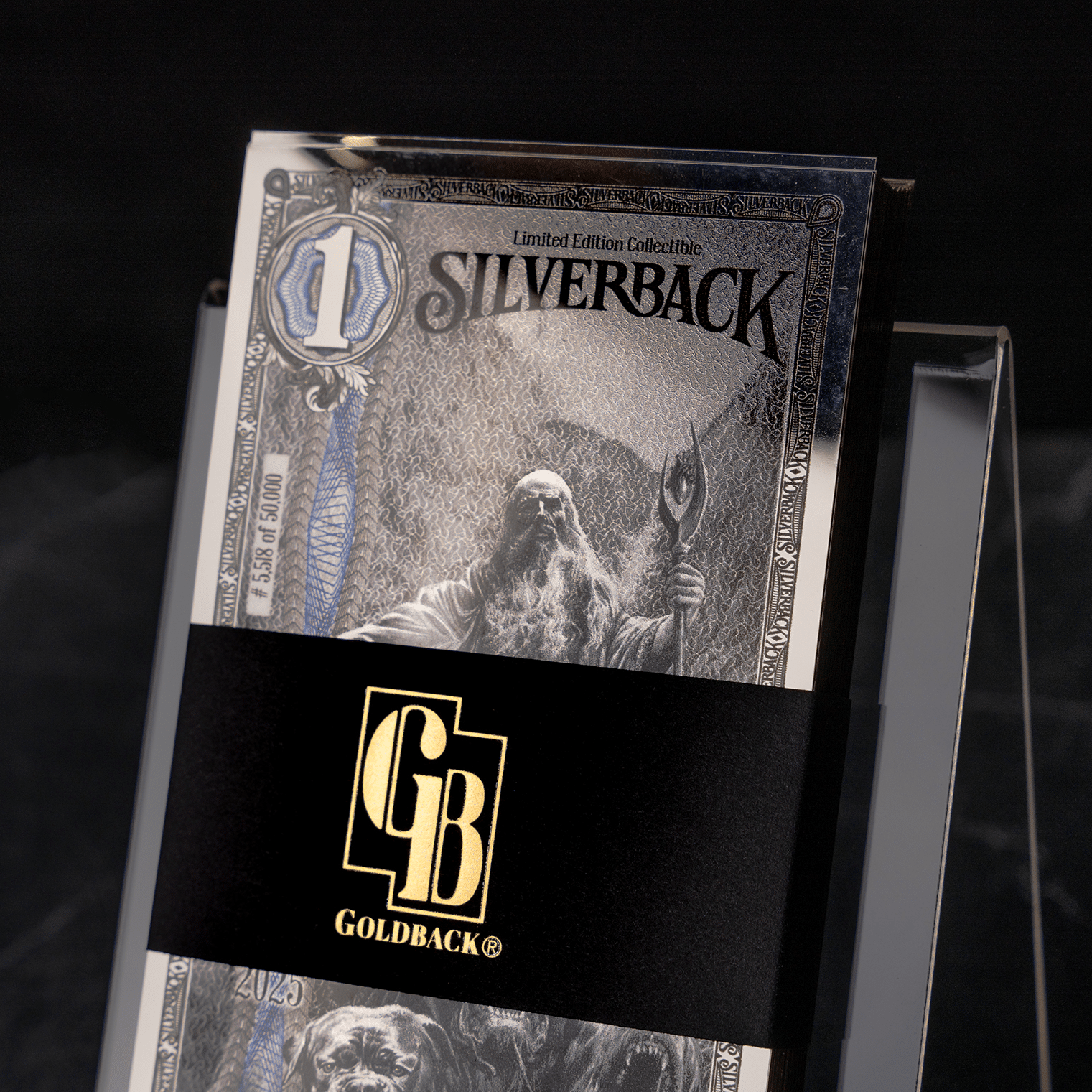

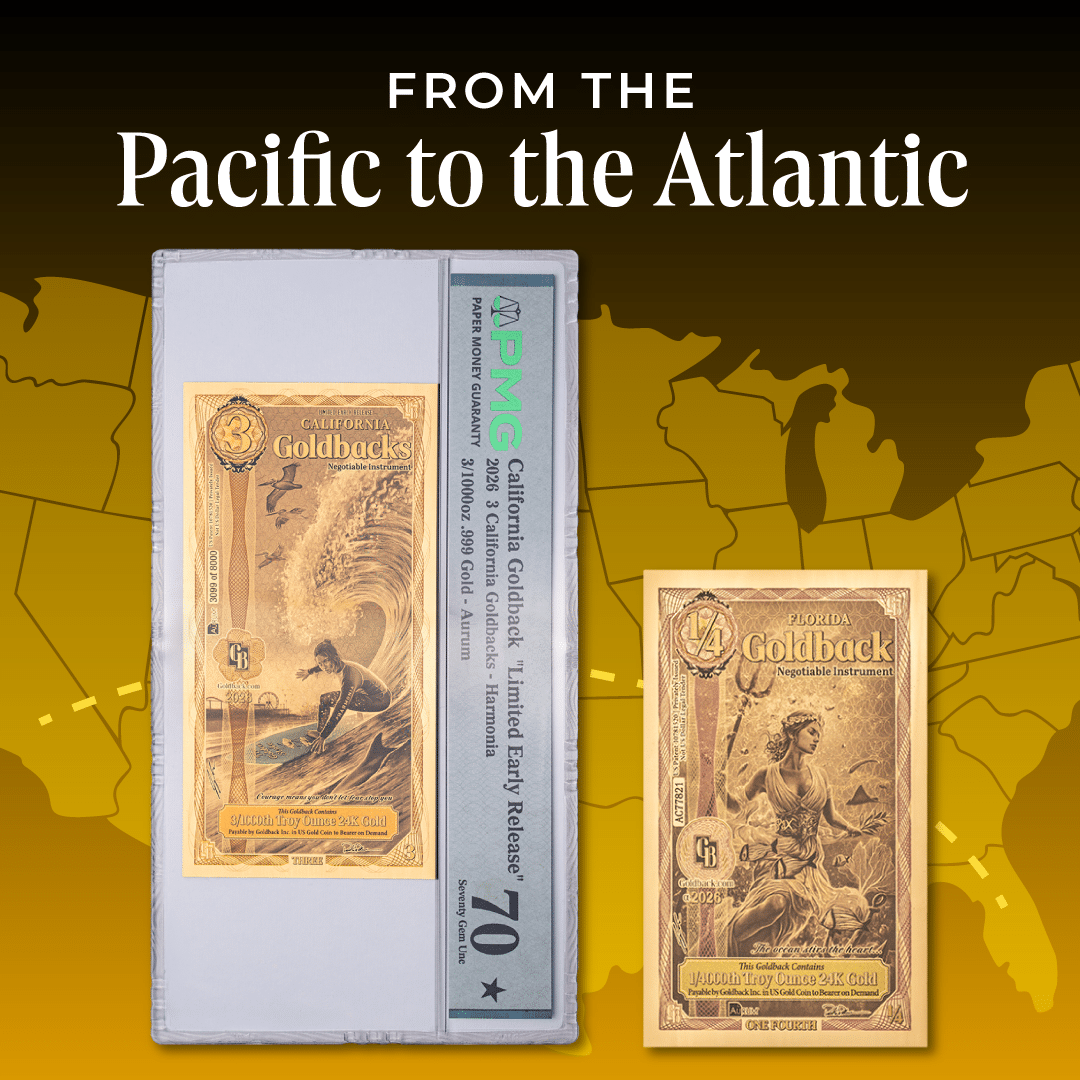

Goldback Inc. was launched in 2019 by founder and CEO Jeremy Cordon. Goldbacks are manufactured by Valaurum using a 5th-generation vacuum-deposition process that bonds 99.9% pure 24K gold between two protective polymer layers. A 1 Goldback holds 1/1,000 of a troy ounce, small enough that a single denomination covers small purchases. As of May 2026, 10 state series are live: Utah, Nevada, New Hampshire, Wyoming, South Dakota, Oklahoma, Florida, Arizona, Idaho, and one more launching in 2026.

What It Is

A complementary, alternative gold currency available in multiple denominations and designed to be spent. Eight active denominations are in circulation: 1/4, 1/2, 1, 2, 5, 10, 25, and 50. The 1/4 Goldback (1/4,000 oz) is the smallest physical gold currency denomination on the market. The 100 Goldback was discontinued, but existing 100s remain valid at participating merchants. The Goldback calculator shows the live exchange rate, which updates daily at 10 AM Mountain Time.

Pros

- The 1/4 Goldback (1/4,000 oz) solves the “gold is too chunky to spend” problem. No silver coin matches that divisibility.

- Real merchant network across 10 state series, with 5,000+ merchants as of May 2026. The network grew 88% in 2025 (1,902 to 3,581) and crossed 5,000 in May 2026.

- Four layers of anti-counterfeit security: UV-reactive ink, serial numbers, crystallization patterns, and raised imagery.

- Manufacturer warranty replaces any Goldback damaged by a production defect. No bullion coin or bar comes with that protection.

- State-specific designs hold collector value beyond spot.

Cons

- The ~100% premium over spot covers the highly complex manufacturing process, Valaurum’s advanced multi-layer anti-counterfeiting technology, and the cost of engineering gold into a form practical for everyday spending — a value no standard bullion coin or bar provides. Unlike a coin or bar sold at melt value, a Goldback spent at a merchant returns the full premium as purchasing power; the cost only lands if you sell it back into USD.

- Merchant density is uneven. Utah, New Hampshire, and Idaho are the strongest. Suburban New Jersey, less so.

- One private company controls supply, the daily exchange rate, and the warranty.

- Polymer wears with heavy handling. The gold content stays intact, but the aesthetic value drops.

Cost & Premium

1 Goldback retails at roughly $9–$10 (gold at ~$4,753/oz in April 2026). The premium funds the vacuum-deposition manufacturing, the multi-layer anti-counterfeiting technology, the merchant network, and the warranty. Spent at a participating merchant, you get the full premium back as purchasing power — the cost only lands if you sell it back into USD. Sold at goldback.com and through authorized dealers including Money Metals Exchange and Alpine Gold.

What Users Say

Reddit’s r/preppers and r/Gold call Goldbacks “legitimate” and “innovative.” One r/Gold commenter put it this way: “100% worth getting, but if you’re getting them in any sizeable amount more than just for novelty, you’ll want to buy from the right places.” Independent dealer Summit Metals confirms the ~100% premium while endorsing the genuine 99.9% gold content. Wikipedia’s Goldback article covers the 2019 launch, the Valaurum manufacturing relationship, and the state-by-state rollout. The Goldback FAQ handles the common skeptic questions.

Best for: Anyone who wants alternative currency they can hand to a cashier — not just stack in a safe.

2. Bitcoin (BTC) — Best for Portable, Hard-Capped Digital Sound Money

Bitcoin is the most portable alternative currency ever invented, and also the most volatile. We sent $200 in BTC across continents in under 12 minutes for a fee of about $0.40. The same value moved by wire would have cost $25 and taken two business days. That’s the pitch. The downside is that the same $200 might be $185 or $215 by the time it arrives.

Bitcoin launched in 2009. There will only ever be 21 million coins. As of April 2026, PayPal’s merchant report says ~40% of US merchants accept some form of crypto, and 50% of large enterprises ($500M+ annual revenue) accept it. But “accepts crypto” almost always means a processor like BitPay or PayPal converts the coin to dollars at checkout. The merchant never holds Bitcoin, and you’ve effectively sold it rather than spent it. Microsoft, Starbucks, and AT&T show up on those lists through that processor layer, not because a cashier takes BTC at the register. Spending Bitcoin in person, hand to hand, is still rare — which is the gap a physical currency like Goldback fills.

What It Is

A decentralized digital currency settled on a public blockchain. No central issuer, no central custodian if you self-custody. Smallest unit is 1 satoshi (1/100,000,000 BTC), which means you can spend fractions of a cent in dollar terms. As Goldback explains, Bitcoin and physical gold currency solve different problems. Bitcoin wins on portability. Goldback wins on physicality.

Pros

- Send any amount, anywhere, in minutes. No bank, no permission.

- Hard cap at 21 million. Inflation-resistant by protocol.

- Self-custody is possible. With a hardware wallet, no one can freeze your coins.

- Massive merchant footprint when you include payment processors like BitPay.

Cons

- Volatility is the dealbreaker for daily spending. Intraday swings of 5–10% happen often.

- Self-custody is hard to do safely. Most users hold on exchanges, which reintroduces counterparty risk.

- On-chain fees spike during congestion — sometimes $20+ for a single transfer.

- Capital gains tax applies to every spend. The IRS treats BTC as property, not currency.

Cost & Premium

Spot price only — no premium over the underlying asset. Network fees range from $0.30 (Lightning) to $20+ (mainchain during peak congestion). Major exchanges charge 0.1–1.5% on buy/sell.

What Users Say

Trust Pilot ratings vary by exchange (Coinbase: 1.5/5, ~6,000 reviews; Kraken: 3.4/5, ~1,400 reviews — most complaints center on support, not the asset itself). Reddit’s r/Bitcoin is largely positive on protocol, mixed on day-to-day spending utility. The Motley Fool’s 2026 inflation-hedge guide lists BTC as a top digital hedge alongside gold.

Best for: Tech-comfortable holders who want a portable, hard-capped digital asset and can stomach the volatility for daily-spend use.

3. USDC — Best for Low-Fee Dollar-Pegged Digital Spending

USDC is the boring stablecoin that quietly does the job. We moved $500 in USDC on the Base network for less than $0.01 in fees and the transaction settled in about 2 seconds. That’s not just faster than a wire — it’s faster than swiping a card. The catch is that you’re trusting Circle to back every token 1:1 with dollars, and Circle can freeze a wallet if asked.

USDC is issued by Circle. Each token is backed by $1 in cash or short-term Treasuries, audited monthly by Deloitte. As of December 2025, USDC and USDT together exceed $200 billion in circulation. USDC is the more US-regulated of the two — Circle is a New York licensed financial institution.

What It Is

A dollar-pegged stablecoin running on Ethereum, Solana, Base, Polygon, and several other chains. Smallest unit is $0.000001. Used widely in DeFi, by remittance apps, and increasingly as a payment rail.

Pros

- Average transfer fee of 0.1–0.15%. Free on Base. Near-free on Solana.

- Backed 1:1 by USD reserves with monthly attestations.

- Programmable money — can be used in smart contracts and DeFi.

- Settlement in seconds, not days.

Cons

- Circle can freeze any USDC wallet on government request. That’s happened, multiple times.

- Not really an “alternative” to the dollar — it’s a digital wrapper around the dollar.

- Network fees on Ethereum mainnet can spike during congestion.

- You need a crypto wallet to hold or spend it. That’s a learning curve for non-tech users.

Cost & Premium

Trades 1:1 with USD. Transfer fees 0.1–0.15% on most chains. No premium over the underlying asset.

What Users Say

Coinbase reviewers (1.5/5, ~6,000 Trustpilot reviews) generally praise USDC stability while complaining about platform support. Crypto industry analysts call USDC the “preferred institutional stablecoin” thanks to Circle’s regulatory posture. MoonPay’s 2025 stablecoin list ranks USDC #2 by market cap behind USDT.

Best for: People who want fast, cheap, dollar-stable digital payments and trust regulated US issuers more than offshore ones.

4. USDT (Tether) — Best for the Cheapest Stablecoin Transfers

USDT is what people in countries with collapsing currencies actually use. We moved $500 in USDT on the Tron network for less than $0.01. That’s the same as USDC on Base, but USDT-on-Tron is what’s running the global remittance corridor right now. From Argentina to Lagos to Manila, it’s the de-facto digital dollar. The catch is regulatory: Tether’s reserve audits are thinner than Circle’s, and the company operates offshore.

USDT is issued by Tether Limited. Total market cap exceeds $130 billion as of late 2025, making it the largest stablecoin and one of the largest cryptocurrencies overall.

What It Is

A dollar-pegged stablecoin running on Tron, Ethereum, Solana, and many other chains. Most volume by far runs on Tron’s TRC-20 network.

Pros

- USDT-on-Tron transfers cost less than $0.01. The cheapest dollar rail anywhere.

- Largest liquidity of any stablecoin — easiest to convert in any country.

- Works on basically every centralized crypto exchange.

- Used heavily in emerging markets where local currency is unstable.

Cons

- Reserve attestations come from BDO, not a Big Four firm. Less transparency than USDC.

- Tether can freeze any USDT wallet, same as Circle with USDC.

- Has lost the peg briefly in 2022. Recovered within hours, but the wobble was real.

- Increasingly facing regulatory pressure in the US and EU.

Cost & Premium

Trades at $1.00 ± 0.001. Tron transfers under $0.01. Ethereum transfers vary with gas. No premium over USD.

What Users Say

Heavy users in remittance markets are positive. US-based crypto regulators are skeptical. BingX’s 2026 commodity stablecoins guide notes that USDT remains the dominant fiat-backed stablecoin despite the regulatory friction. Reddit sentiment splits: r/cryptocurrency leans cautiously positive on USDT for transfers, more skeptical on it as a long-term store.

Best for: International users who need the cheapest, deepest dollar-rails and accept the offshore regulatory profile.

5. PAX Gold (PAXG) — Best for Tokenized Gold with US-Regulated Custody

PAXG is gold for people who never want to touch gold. Each PAXG token represents the legal title to one troy ounce of LBMA Good Delivery gold sitting in a Brink’s vault in London. We bought 0.01 PAXG (~$47) on Coinbase, paid about $0.50 in trading fees, and the price tracked spot gold within 0.2% all afternoon. Then we tried to sell it back. That part worked too, and we never had to ship a coin.

PAXG is issued by Paxos Trust Company, regulated by the New York State Department of Financial Services. As of December 2025, PAXG’s market cap stands near $1.6 billion.

What It Is

An ERC-20 token on Ethereum where 1 PAXG = 1 troy oz of allocated, vaulted, LBMA-certified gold. Smallest tradable unit is 0.01 PAXG (~$47 at April 2026 prices). Holders can technically redeem 430 PAXG for a full physical gold bar — and Paxos’s partner network handles smaller physical redemptions too.

Pros

- Backed 1:1 by allocated physical gold. Monthly attestations published.

- Regulated by NYDFS, the strongest US regulatory profile of any tokenized gold.

- 0.02% on-chain transfer fee. Far cheaper than physical gold transport.

- Tradable on Coinbase, Kraken, and most major US exchanges.

Cons

- Not a payment rail. You can’t spend PAXG at a coffee shop. You sell it first.

- Ethereum gas fees apply on every transfer. Sometimes meaningful.

- Custody risk lives with Paxos. If they fail, your gold claim depends on the bankruptcy process.

- Capital gains tax on every sale, just like physical gold.

Cost & Premium

Trades within ~0.5% of spot gold. 0.02% on-chain fee. 1.00% conversion fee for amounts between 2 and 25 PAXG via Paxos directly (lower for larger transactions). Until March 31, 2026, Paxos waived the creation fee — standard rates apply after.

What Users Say

Coinbase users rate PAXG 4.5/5 on the asset page (mainly for transparency and price tracking). Crypto Twitter generally calls PAXG the “safer of the two big tokenized gold tokens.” Datawallet’s gold-backed crypto rankings put PAXG at #1 for regulatory profile.

Best for: Crypto-comfortable holders who want clean exposure to physical gold without storage logistics.

6. Tether Gold (XAUT) — Best for Tokenized Gold at the Lowest Premium

XAUT is PAXG’s offshore cousin and currently the largest tokenized gold token by market cap. We watched XAUT trade at ~$4,308/oz one afternoon while PAXG sat at ~$4,318. That ~$10 spread isn’t always there, but XAUT does tend to trade slightly closer to spot than PAXG. The trade-off is the regulatory profile: XAUT’s issuer operates under El Salvador’s National Commission of Digital Assets, not New York.

XAUT is issued by TG Commodities Limited, an affiliate of Tether. As of December 2025, XAUT’s market cap exceeds $2.2 billion, making it the largest tokenized gold asset.

What It Is

An ERC-20 token where 1 XAUT = 1 troy oz of LBMA Good Delivery gold held in Switzerland. Smallest tradable unit is 0.000001 XAUT (effectively dust-level fractional ounces).

Pros

- Tends to trade marginally cheaper than PAXG — closer to spot gold.

- Largest tokenized gold market cap (~$2.2B) means the deepest liquidity.

- Same fundamental product as PAXG — 1:1 backed allocated gold.

- Lower premiums than physical gold during 2026 supply tightness.

Cons

- Issuer is Tether-affiliated, regulated offshore (El Salvador’s CNAD).

- Physical redemption requires 430 XAUT minimum and you arrange Swiss pickup yourself.

- Same custody-risk and tax treatment as PAXG.

- Less common on US exchanges — KuCoin and Bitfinex carry it; Coinbase doesn’t.

Cost & Premium

Trades within ~0.3% of spot gold. ERC-20 gas fees apply. Slight discount to PAXG most days.

What Users Say

Crypto analysts split on PAXG vs. XAUT mostly along regulatory lines. Gate.com’s 2026 comparison notes that XAUT wins on raw market cap and pricing while PAXG wins on US regulation and accessible redemption. BingX’s tokenized gold breakdown calls it “the closest to spot you can get without buying a bar yourself.”

Best for: International crypto holders who want the largest, lowest-premium tokenized gold market and accept offshore regulation.

7. American Silver Eagle 1 oz — Best for Government-Minted Physical Silver

The American Silver Eagle is the closest thing to a Constitutional silver standard the US still mints. We picked one up from Monument Metals at $79.77, about a 5.4% premium over melt at silver’s April 2026 spot of ~$75/oz. It’s the most-recognized silver bullion coin in the world. It’s also impossible to spend at a 7-Eleven, because no cashier in 2026 has any way to value it.

The US Mint has produced the American Silver Eagle continuously since 1986. The 1 oz coin contains 1.000 troy oz of .999 fine silver and carries a $1 face value — legal tender by name only.

What It Is

A 1 oz pure silver bullion coin produced by the US Mint. Sold by every major dealer (JM Bullion, APMEX, SD Bullion). The $1 face value is symbolic.

Pros

- Recognized by every US precious metals dealer on sight.

- US Mint quality and pedigree. No authentication required at major dealers.

- Eligible for Precious Metals IRAs.

- Lower premium than most government-minted coins (5–8% over melt).

Cons

- Can’t spend at retail. The $1 face value is a fiction relative to the ~$80 silver value.

- Requires a dealer or buyer to convert back to USD. Not instant.

- Bulky relative to value compared to gold or stablecoins.

- Counterfeit risk on the secondary market.

Cost & Premium

April 2026 dealer pricing: $79.77 (Monument Metals) to ~$86 average across 13 dealers. ~5–8% premium over silver spot.

What Users Say

Silver Eagle stackers on r/Silverbugs treat the coin as the standard “first piece” buy — Trustpilot data on JM Bullion (4.6/5, 1,385+ reviews) reflects steady satisfaction with shipping and packaging. Common complaint: post-2021 reverse design changes drew mixed reviews from collectors who preferred the original 1986 walking-Liberty pairing.

Best for: Stackers who want recognized US-government silver and don’t need to spend it directly.

8. Junk Silver (Pre-1965 90% Silver Coins) — Best for Melt-Value Barter-Tier Silver

Junk silver is what survives if the dollar doesn’t. We bought a $10 face value bag of pre-1965 quarters and dimes for about $570 (~7% over melt at spring 2026 prices). Each dime contains ~0.0715 oz of 90% silver. That’s small enough to barter for groceries, big enough to actually move value. No serial numbers, no certificates, no fuss.

“Junk silver” refers to pre-1965 US dimes, quarters, and half-dollars minted in 90% silver / 10% copper. The name comes from collectors. These coins carry no numismatic premium, just metal value.

What It Is

US-minted 90% silver coinage that retains legal-tender status at face value (a junk silver dime is still 10 cents). Sold by face-value bag at every major bullion dealer. $1 face value = ~0.715 oz of pure silver.

Pros

- Lowest premium over spot of any physical silver — 5–12% above melt.

- Highly divisible. A single dime is ~0.07 oz of silver, ideal for small barter.

- Recognizable by anyone old enough to remember pre-1965 coinage. No authentication needed.

- Constitutional-silver framing carries weight with sound-money buyers.

Cons

- Same retail-spending problem as Silver Eagles. No cashier weighs coins.

- Coin condition varies widely. Worn coins still trade at melt, but you’re paying for silver, not numismatic appeal.

- Bulkier than rounds or bars per dollar of silver.

- Some buyers want bullion only and won’t take coins.

Cost & Premium

April 2026: $10 face value bag runs ~$570 at SD Bullion and Money Metals Exchange. That’s a 5–12% premium over melt depending on dealer and quantity.

What Users Say

Money Metals Exchange reviewers call junk silver “the survivalist’s silver” and consistently praise the low premium. r/Silverbugs on Reddit treats junk silver as the standard recommendation for new stackers. The Bullion Bank’s 2026 guide calls it the most efficient form of physical silver you can hold.

Best for: Sound-money buyers who want melt-value silver in barter-friendly small denominations.

9. American Gold Eagle 1/10 oz — Best for Fractional Government-Minted Gold

The 1/10 oz American Gold Eagle is the smallest US-government-minted gold coin you can buy. And you still can’t spend it at a coffee shop. We pulled one off JM Bullion at ~$579 in April 2026, with gold at ~$4,753/oz. The coin’s $5 legal-tender face value is meaningless at checkout. Every dealer in the US will buy it on sight, which makes it the fastest exit-to-USD on this list. But exiting to USD isn’t the same as spending.

The 1/10 oz American Gold Eagle is 22K (91.67% gold), produced by the US Mint since 1986. The copper-and-silver alloy makes it more scratch-resistant than .9999 fine coins.

What It Is

A 1/10 troy oz fractional gold bullion coin produced by the US Mint. Carries a $5 legal-tender face value (a fiction). Eligible for Precious Metals IRAs.

Pros

- Every US bullion dealer buys it on sight. No authentication friction.

- 22K alloy resists scratches better than .9999 coins. Capsule storage isn’t critical.

- Most recognized fractional gold coin in the US.

- IRA-eligible by Congressional authorization.

Cons

- Can’t spend at retail. The face value is symbolic.

- Premium of ~22% over spot is high. Ten 1/10 oz Eagles cost ~10–15% more than a single 1 oz Eagle.

- Counterfeit market exists. Buy from major dealers only.

- Same liquidation friction as any physical gold — you need a buyer.

Cost & Premium

April 2026 wire price at JM Bullion: ~$579 per coin. ~22% premium over spot. Free shipping over $499.

What Users Say

JM Bullion: 4.6/5 across 1,385+ Trustpilot reviews. APMEX: 1.7/5 across 7,900+ reviews, dominated by shipping delays and a 2025 counterfeit-silver incident. The coin itself earns steady “easy to resell anywhere” praise across both platforms, with reviewers consistently noting the 22K alloy holds up better in pocket carry than .9999 fine alternatives.

Best for: Stackers who want US-government fractional gold and value domestic recognition over purity or premium.

10. Glint Pay — Best for Spending Gold Through a Mastercard

Glint Pay is the digital answer to “how do I actually pay with gold at a normal store?” We loaded $200 into the app, converted it to gold at a 0.5% fee, and paid for groceries with the physical Mastercard. The merchant saw a normal card transaction. We saw our gold balance drop by the dollar value. The trade-off is custody: Glint holds the gold for you. If they fail, your claim depends on insurance and the bankruptcy process.

That trade-off is also why Glint lands at #10 despite near-universal acceptance. On raw spendability it scores at the top of the list. But it’s the least currency-like option here: you never hold the gold, and every purchase quietly sells it for dollars at the register, which is a taxable event in the US, not a gold-for-goods trade. Our rubric weights spendability the heaviest, but it docks counterparty risk just as hard, and Glint puts all of that risk on a single custodian. It ranks where it does because of how it works, not because of who makes it.

Glint launched in 2018 and operates in the UK, Europe, and the US. Glint is rated 4.5/5 on Trustpilot across 3,300+ reviews.

What It Is

A mobile app and Mastercard debit card that lets you hold physical gold (allocated and stored in Brink’s vaults in Switzerland) and spend it at any merchant that accepts Mastercard. Conversion happens at point-of-sale.

Pros

- Spend gold at any Mastercard-accepting merchant. Effectively universal merchant network.

- 0.5% conversion fee on every gold transaction.

- Allocated, insured, vaulted physical gold backing.

- Can also hold and spend USD, GBP, EUR, and silver.

Cons

- 3% fee on debit/credit card deposits. Use ACH (free) instead.

- $10 physical card fee.

- Custody risk lives with Glint. Vault insurance is real, but bankruptcy could complicate access.

- Not legal tender — every spend triggers a sale of gold (capital gains tax applies in the US).

Cost & Premium

Buy gold at near-spot (small spread). 0.5% per gold-funded transaction. 0.02% monthly storage fee. ATM withdrawals: $1.50.

What Users Say

Trustpilot reviewers (4.5/5, 3,300+ reviews) praise the “actually-spend-gold” experience and the mobile app. The recurring complaint is the 3% deposit fee on cards. The College Investor’s Glint review calls it “the closest you’ll get to a gold checking account.”

Best for: People who want digital gold custody with universal merchant acceptance and accept the 0.5% transaction fee.

11. BerkShares — Honorable Mention (Local Fiat, Not Gold)

BerkShares is included for honesty about what alternative currency means. It’s not gold. It’s not crypto. It’s a paper local currency printed in the Berkshires region of Massachusetts and accepted at ~300 businesses there. It’s redeemable 1:1 with USD at Lee Bank and Pittsfield Cooperative. The case for including it is simple: BerkShares is the most successful US local currency by merchant adoption, and it shows what a hyperlocal alt currency actually looks like at scale.

BerkShares launched in 2006 and went digital in 2022.

What It Is

A local currency note (and digital balance) backed 1:1 by USD held in regional banks. Used only in the Berkshires.

Pros

- Universal acceptance within the Berkshires (~300 businesses).

- No transaction fees for merchants — bypasses card processors.

- 1:1 USD-backed, so no volatility.

- Strong local-economy story.

Cons

- Not gold. Tracks the dollar all the way down.

- Geographically locked to one region.

- 1.5% redemption fee when banks convert BerkShares back to USD.

- Doesn’t solve the inflation-hedge problem at all.

Cost & Premium

1 BerkShare = $1 USD. No premium. 1.5% fee when redeeming back at a bank.

What Users Say

The Boston Globe and WBUR have both run profiles praising the merchant-fee savings and the local-economy effect. Critics note that BerkShares doesn’t hedge inflation because it’s just dollars in different paper.

Best for: Berkshires residents who want to support local businesses and don’t need an inflation hedge.

FAQs

What is the best alternative currency to the US dollar?

It depends on what you want it to do. For physical, fractional, spendable currency, Goldback is the only product that fits all four criteria. For digital portability, Bitcoin wins. For low-fee dollar-stable transfers, USDC and USDT lead. For pure store of value, physical gold and silver bullion remain the standard. Most sound-money buyers hold a mix: Goldback for spending, bullion for stacking, BTC for portability. See our breakdown of the benefits of using alternative currency over cash for the deeper case.

Can you actually spend gold at a store?

Yes, but only one product on this list lets you do it physically without converting first. Goldback is accepted at 5,000+ merchants across 10 state series (Utah, Nevada, NH, Wyoming, SD, Oklahoma, Florida, Arizona, Idaho, plus one more launching in 2026). Glint Pay lets you spend gold via a Mastercard at any retailer, but converts to dollars at the point of sale. Physical gold coins like Eagles can’t be spent at retail. You have to liquidate them first.

Bitcoin vs. Goldback: which is better as a currency alternative?

They solve different problems. Bitcoin is the most portable digital currency ever invented. You can send any amount, anywhere, in minutes. Goldback is the most spendable physical gold currency. You can hand it to a cashier today. Bitcoin’s volatility makes it hard to use as a daily medium of exchange. Goldback’s geographic concentration limits where it’s frictionless. Many holders use both, for different reasons. See Goldback vs. cryptocurrency: 4 key differences for the full breakdown.

Are stablecoins like USDC and USDT really alternative currencies?

Technically, no. They’re digital wrappers around the US dollar. They share the dollar’s risk (inflation, monetary policy) and don’t hedge against fiat debasement. But they do solve the “cheap, fast digital payment” problem better than banks. If your goal is to avoid the dollar entirely, stablecoins won’t help. If your goal is to move dollars cheaply and globally, they’re the best tool out there.

What’s the smallest amount of gold you can actually spend?

The 1/4 Goldback (1/4,000 oz, ~$2.50 in gold value at April 2026 prices, retail ~$2.50) is the smallest physical gold currency on the market. Glint Pay can spend $1 in gold via card. Tokenized gold (XAUT, PAXG) is divisible to dust-level fractional ounces but you have to sell first. Standard bullion’s smallest unit is the 1g bar (~$152) or the PAMP 1g Lady Fortuna (~$220), neither of which is meant to be spent at retail.

Final Verdict

For people skeptical of fiat: Goldback is the strongest pick if you want a physical, fractional, spendable alternative, and you want to support a sound-money product without converting back to dollars at point-of-sale. Bitcoin is the runner-up if you’d rather hold a digital asset and can stomach the volatility. If you just want a hedge to stack and forget, junk silver or 1/10 oz Gold Eagles win on premium-to-storage ratio. Most of our readers end up holding a mix. Start with the Goldback merchant directory and see if there’s one near you, or read our case for spendable gold currency if you’re new to the category.